The RedBook Insider: The Value Gap Reshaping Australia’s New Car Market

Two data points emerging from the latest VFACTS May 2026 segmentation analysis tell a compelling story about the rapid rise of Chinese-affiliated brands in Australia - and critically, about what legacy manufacturers have misjudged to their own detriment.

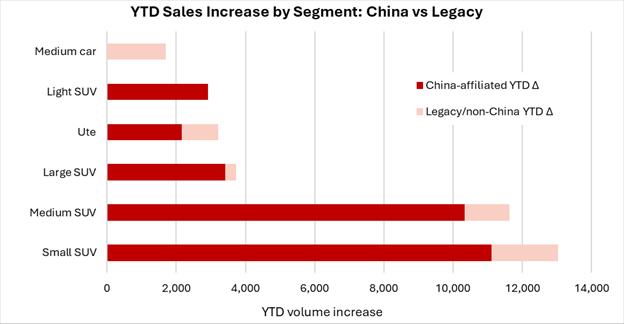

The first chart below clearly illustrates where momentum sits. Using the top 50 selling models from May 2026 YTD, China-affiliated brands are driving disproportionately strong volume growth across high-demand segments, particularly in small SUVs, medium SUVs and light commercial vehicles. In contrast, legacy manufacturers are showing comparatively modest gains, and in some segments, outright stagnation.

Source: VFACTS & EVC

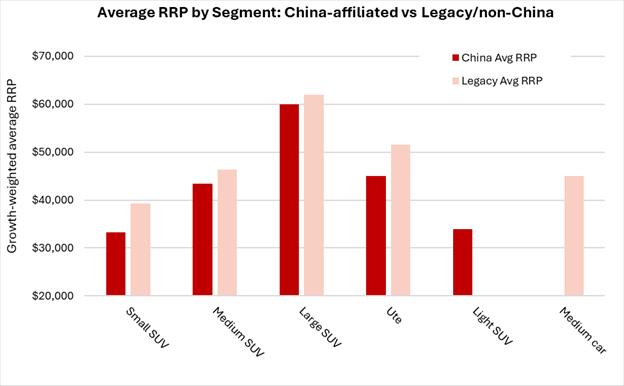

The second chart following provides the missing context. Across nearly every comparable segment, Chinese-affiliated brands are entering the market at materially lower average recommended retail prices, with equivalent and even superior specification in many instances. This price difference is creating structural change.

Source: RedBook, VFACTS & EVC

Taken together, these charts highlight a decisive shift in market dynamics. This more than simply a case of new entrants gaining traction through novelty or supply availability - it is a textbook response to a widening value gap.

Importantly, this is not simply a story about cheaper Chinese EV powertrains undercutting the market. Since COVID, legacy mainstream brands have systematically increased recommended retail prices - driven by supply chain cost recovery, electrification investment pass-through, specification uplift strategies and margin optimisation. Models that were once priced as accessible volume sellers have migrated upward, in many cases by thousands of dollars. The value-for-money equation that defined brands like Hyundai, Kia, Nissan and Mitsubishi a decade ago has fundamentally shifted. Chinese-affiliated manufacturers have recognised this gap and moved decisively to fill it - across both ICE and EV powertrains - restoring a value proposition that the market was missing.

For RedBook’s customer base - insurers, financiers, fleet managers, dealers and alike - this shift carries direct commercial implications. Residual value forecasting must now account for accelerating competitive pressure in segments where legacy brands once held pricing power unchallenged. Insurers face evolving risk profiles as the parc composition shifts toward newer, less established brands with different parts supply chains and repair cost structures. Financiers and fleet operators need to reassess total cost of ownership assumptions as Chinese-affiliated brands increasingly compete not just on sticker price but on warranty, specification and running costs. For dealers, the message is equally clear: brand loyalty is being tested by value, and the showroom battle is increasingly being won on price-to-spec ratios rather than badge heritage.

The rise of Chinese-affiliated brands is not disruption for disruption’s sake. It is the market correcting for a value gap that legacy brands created. For those in the business of pricing, insuring and financing vehicles, understanding this dynamic is no longer optional - it is essential.

Recent Posts

-

The RedBook Insider: The Value Gap Reshaping Australia’s New Car Market3rd July 2026

The RedBook Insider: The Value Gap Reshaping Australia’s New Car Market3rd July 2026 -

The RedBook Insider: ADAS Fitment is Surging - But the Risk Pool Is Still Stuck in the Past3rd July 2026

The RedBook Insider: ADAS Fitment is Surging - But the Risk Pool Is Still Stuck in the Past3rd July 2026 -

The RedBook Insider: Heavy Thinking: Are We Ready for the Weight of Electrification?3rd July 2026

The RedBook Insider: Heavy Thinking: Are We Ready for the Weight of Electrification?3rd July 2026