The RedBook Insider: RedBook 2030: Will Fuel Volatility Shift the Powertrain Mix Sooner

With pump prices in capital cities pushing $2.50/L amid Middle East supply uncertainty, Australia has been handed a real-world stress test for the economics of powertrain choice. It’s also a timely checkpoint for the RedBook 2030 Powertrain Forecast, a model built before the latest supply-side shocks, and one that already anticipates a steady transition to New Energy Vehicles (NEVs), with an exponential inflection post-2030.

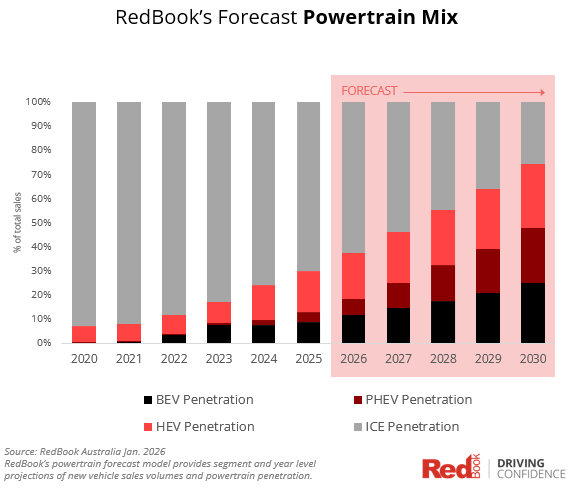

The chart below shows the ICE share stepping down as HEV, PHEV and BEV take a growing slice of total sales. In the context of fuel volatility, it’s a helpful way to visualise where a shorter EV payback period could pull forward the mix shift especially in segments with high annual kilometres.

The question is whether today’s price environment simply compresses near-term timelines or whether it signals something more structural. The carsales Australian Car Buyer Report 2026 certainly suggests intenders are considering EVs more and more. Though just last week this curiosity spiked further, taking a +76% jump in searches for EV on the platform which sends a pretty strong signal that car buyers are looking to escape rising running costs in any way possible.

1) Total cost of ownership (TCO): the payback clock just sped up

Fuel price is the fastest-moving variable in TCO. When petrol rises, the operating-cost advantage of EVs grows immediately and the payback period for the higher purchase price shortens for both fleets and private buyers. If elevated prices persist, that dynamic can pull demand forward into the 2026-30 forecast window shown in the chart, bringing our post-2030 inflection closer.

- Higher per litre reduces payback time for high-kilometre users first (fleet, regional commuters, rideshare).

- Purchase-price sensitivity remains, but the operating-cost delta becomes harder to ignore.

2) Why PHEVs matter more in volatile conditions

Whilst EV purists might denigrate them, our forecast positions Plug-in Hybrids (PHEVs) as a critical bridging technology especially while some consumers remain cautious about EV range, towing needs, and charging access. Volatility tends to reinforce the appeal of an electric-first driving cost per kilometre, without forcing a full behavioural shift on day one. In addition, notable new entrants include Chery's pioneering diesel PHEV, which is scheduled for launch this year, further supports:

- PHEVs can capture meaningful fuel savings on urban duty cycles.

- They provide a practical hedge against both fuel spikes and charging constraints.

3) ICE phase-out is not linear and not uniform by segment

Fuel pricing can move the market, but segment requirements still set the ceiling. Passenger vehicles are typically the most responsive to fuel-cost shocks, while capable SUVs and Light Commercial Vehicles (LCVs) show more persistence due to “fit for purpose” application such as payload, range, towing, duty-cycle and/or charging access needs. Our data suggests these segments will maintain a sustained presence well beyond the passenger-car inflection including a niche but durable demand for high-output internal combustion options.

4) Asset lifecycle and depreciation: the secondary-market impact

As NEV penetration increases, depreciation profiles are likely to shift. Faster technology cycles, policy signals, and changes in operating-cost expectations can accelerate obsolescence risk for traditional ICE assets especially where fuel prices remain elevated or volatile.

- Residual-value assumptions may need greater sensitivity to energy-price scenarios.

- Fleet replacement strategies may tighten to avoid value cliffs.

The strategic question

Does the current volatility warrant a fundamental update to our 2030 powertrain outlook or are we seeing a temporary spike that will settle as supply chains normalise? Either way, the market signal is clear: energy prices can accelerate adoption faster than infrastructure or policy alone.