The RedBook Insider: NVES compliance bites as Ute demand holds firm

The New Vehicle Efficiency Standard (NVES) moved from policy to commercial reality on 1 July 2025, when the first compliance performance period began. Almost 9 months on, the early signals are clear: NVES is already influencing the powertrain mix strategies OEMs bring to Australia but it’s doing so in a market where utes and heavy-duty, fit-for-purpose vehicles remain central to buyer demand.

What NVES has changed already: emissions are now a balance-sheet line item

The NVES framework effectively turns fleet-average CO2 performance into a tradable cost: brands that exceed their target can accrue a liability (and ultimately face a penalty), while brands that beat target can generate credits. The NVES Regulator’s first published performance-period results for 2025 (covering 1 July to 31 December 2025) has increased transparency on which OEM model mixes are tracking above or below target and that transparency is flowing quickly into product and pricing decisions.

- Pricing and grade rationalisation: NVES increases the incentive to re-price high-emitting variants, adjust option structures, or steer buyers toward lower-emitting grades where possible.

- A faster pivot to HEV/PHEV: hybrids and plug-in hybrids offer near-term CO2 reduction without relying entirely on Australia’s uneven charging footprint and can be deployed within existing nameplates.

- Mix management becomes a sales lever: allocation, marketing and dealer incentives can shift toward powertrains that improve fleet averages.

- Credits become a strategic hedge: brands may plan to buy credits (or bank their own) as a bridge while waiting for next-generation platforms to arrive.

Winners, losers, and the artificial leg up

Measured locally by way of interim emissions values (IEVs) NVES penalises car-makers that exceed fleet-average CO2 limits while rewarding those that come in under the mandated thresholds. In practice, NVES can create a real competitive advantage for brands with an EV/low-emissions-heavy line-up (or strong hybrid/PHEV mix) as evidence by Tesla in the US, because they’re more likely to beat their fleet targets and generate credits while brands weighted to high-emitting SUVs, Utes and performance models can accumulate liabilities. That’s not necessarily “artificial” so much as “designed”: the mechanism intentionally rewards lower-emissions supply and makes higher-emissions mix more expensive.

- Brands with deep EV portfolios may be able to monetise credits: for example, reporting has highlighted that EV-heavy brands (such as BYD) are positioned to sell NVES credits to other OEMs.

- Brands with emissions-intensive mixes face faster commercial pressure: early reporting on the first NVES results points to several OEMs facing material liabilities where their sales skew to higher-emitting models.

- Flow-on effects can reshape competition: price moves, delayed/limited supply of higher-emitting variants, and a sharper push toward hybrids/PHEVs can shift share at the margin even if underlying Australian demand still favours Utes and large SUVs.

For more detail on which brands hold the cards by way of IEV credits, our compatriots over at carsales have compiled a nice summary of who’s in the red and those with the upper hand.

The market reality check: Utes still sell in huge numbers

Even as OEMs recalibrate for NVES, Australia’s preference for SUVs and Utes continues to dominate the national sales chart. VFACTS reporting for 2025 shows another record year of new-vehicle sales, with the Ford Ranger finishing as Australia’s top-selling vehicle (56,555 units) for the third year running; a signal that the workhorse Ute remains a cornerstone purchase, not a niche indulgence. Early 2026 results reinforce the theme: February 2026 VFACTS reported 90,712 registrations for the month, with Ranger (4,325) and HiLux (3,625) again leading the model rankings.

- Utility-first buying: for many households and businesses, towing, payload, range and serviceability outweigh fuel-efficiency gains.

- Supply constraints: even willing buyers may find limited fit-for-purpose BEV/PHEV options in the 4x4 Ute and heavy-duty van space.

- NVES tension point: these high-volume, higher-emitting segments can quickly drive an OEM’s fleet average in the wrong direction.

Residual values are reinforcing the “fit-for-purpose” thesis

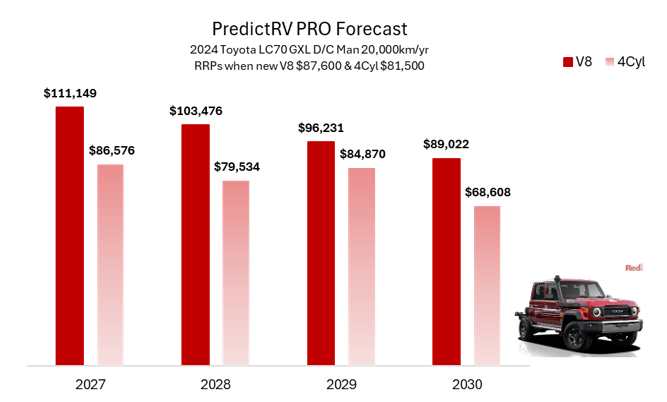

In our July RedBook Insider newsletter, we flagged the risk that policy pressure and limited replacement options could elevate residual values for specific, mission-critical vehicles. Six months into the NVES penalty window, that theme is being echoed in the broader market narrative: multiple industry outlets have reported sharp rises in used LandCruiser 70 Series pricing, particularly around V8-powered variants (no longer available), but even for the far less muscular but potent 4 cylinder on the back of ongoing demand for proven heavy-duty capability. Tools like RedBook’s industry leading PredictRV PRO illustrate how profound this “future classic” type residual positoin could be and it isn’t just isolated to Toyota.

- Scarcity premium: when supply is limited and a vehicle is perceived as “last of its kind”, buyers often pay up; and the used market follows.

- Few true substitutes: for applications where capability is non-negotiab le (remote work, mining support, severe off-road, heavy towing), buyers can’t easily switch to a smaller or lighter platforms.

- Fleet and business continuity: operators may accept higher acquisition and running costs to protect uptime and operational suitability.

So when do we get a highly efficient replacement for the icons?

The gap isn’t a lack of intent; it’s physics, infrastructure and product cadence. A genuine LandCruiser/Ranger Super Duty/Ineos-style replacement needs to deliver payload, towing, long-distance range under load, genuine off-road capability and rapid refuelling/charging in remote conditions. Battery-electric solutions in this space face trade-offs around weight, cost and range when working hard, while PHEV options are emerging but still limited in model availability and configuration. Some local retrofit programs (often targeted at mine sites) hint at what’s possible, but broad-scale, showroom-ready solutions at volume are still in transition.

Summary

NVES is already doing what standards are designed to do; pushing OEMs to re-think their model mix and accelerate lower-emissions powertrains. But Australia’s vehicle demand is still anchored in utility-led segments where fit-for-purpose alternatives remain scarce, and early-2026 VFACTS model rankings continue to be led by Utes. The next 12-24 months will be telling: do we see meaningful increases in PHEV/HEV availability in Utes and heavy-duty SUVs, or does the compliance pressure simply re-price the vehicles Australians keep buying?