The RedBook Insider: 2025’s Brand Value Leaders Revealed: See Which Auto Brands Outpaced the Pack

Toyota, Hyundai & Ferrari Set the Pace in 2025

RedBook’s Marque Equity Index highlights the automotive brands leading (and lagging) in market sentiment and value retention, showcasing those capturing industry confidence and those facing new challenges in 2025 and beyond.

What is the Marque Equity Index (MEI)?

The RedBook MEI is a proprietary metric that quantifies the relative strength of automotive brands in the Australian market. It distils complex market dynamics into a single, understandable score, enabling industry professionals to confidently compare brands. MEI is updated regularly to reflect current market conditions, providing actionable insights for pricing, inventory management, and strategic planning.

How is MEI Calculated?

- Data Sources: MEI draws on RedBook’s extensive database of retail, private, wholesale, and trade-in transaction data, including auction results, dealer sales, and fleet disposals.

- Sales-Weighted Approach: Each brand’s score compares the average retained value of its vehicles against the segment average, adjusted for sales volume and model mix.

- Index Interpretation: MEI scores show how a brand’s value retention compares to direct competitors within the same segment, highlighting relative strengths and weaknesses.

Market Overview

The 2025 RedBook MEI reveals an evolving environment for automotive brand equity in both mainstream and premium segments. Brand equity remains a key factor influencing residual values, fleet decisions, and dealer operations. This year’s results show significant movements across brands, emphasizing the importance of strategic brand management and adaptability.

Mainstream Segment: Winners and Challengers

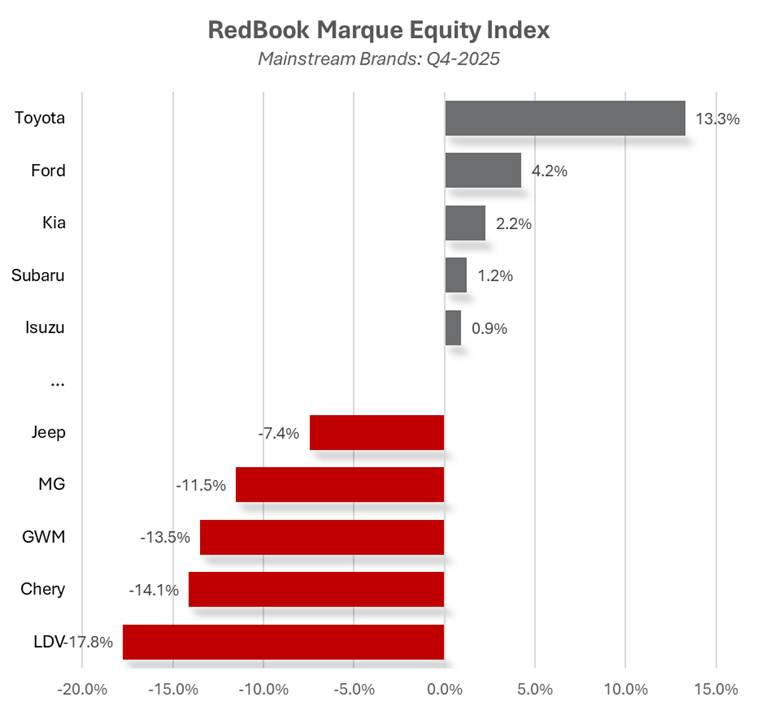

The mainstream market is shaped by both emerging and established players. LDV, Chery, GWM, MG, and Jeep occupy the bottom five positions, with LDV at -17.8%, reflecting ongoing challenges in price retention. These brands face headwinds from market perception, supply chain volatility, and competition.

Toyota leads with a 13.3% index value, reinforcing its reputation for strong residuals and dealer confidence. Ford, Kia, Subaru, and Isuzu also show positive momentum, indicating effective product strategies and sustained demand.

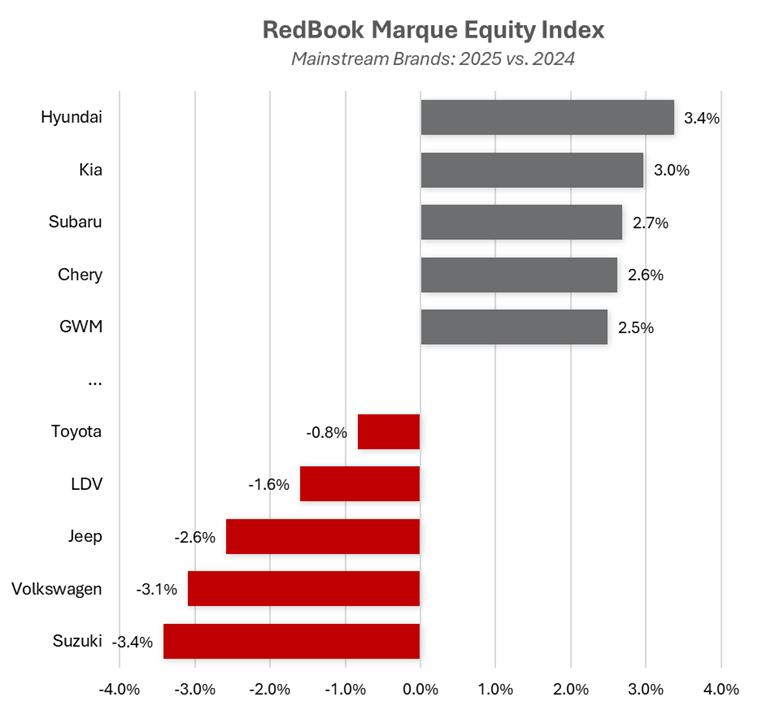

Year-on-year, Suzuki, Volkswagen, Jeep, LDV, and Toyota saw modest declines, while GWM, Chery, Subaru, Kia, and Hyundai posted gains, suggesting some brands are consolidating while others leverage new models or strategies.

Premium Segment: Performance and Prestige

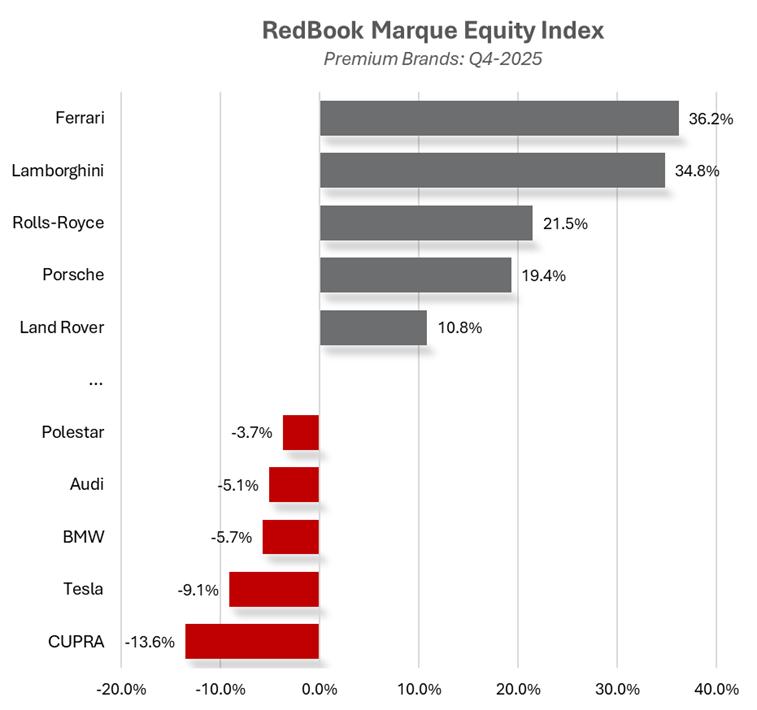

The premium segment remains dynamic, with CUPRA, Tesla, BMW, Audi, and Polestar at the bottom, and CUPRA showing the largest drop at -13.6%. These results reflect product lifecycle timing, stock volume, and broader economic influences.

Ferrari leads with a 36.2% index, followed by Lamborghini, Rolls-Royce, Porsche, and Land Rover. These brands benefit from exclusivity, global demand, and strong dealer networks.

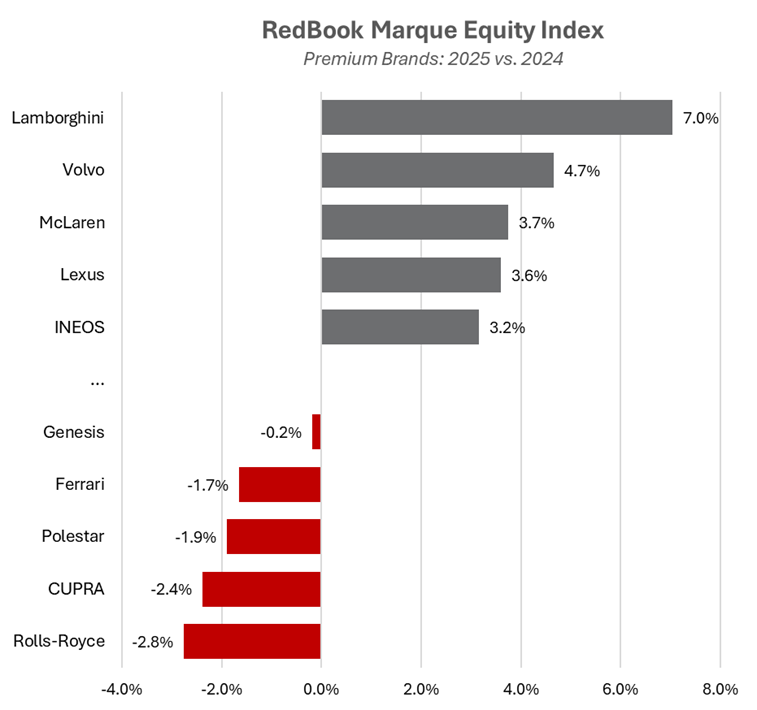

Over the past year, Rolls-Royce, CUPRA, Polestar, Ferrari, and Genesis recorded modest declines, while INEOS, Lexus, McLaren, Volvo, and Lamborghini achieved gains, highlighting the need for strategic brand management and distinctive offerings.

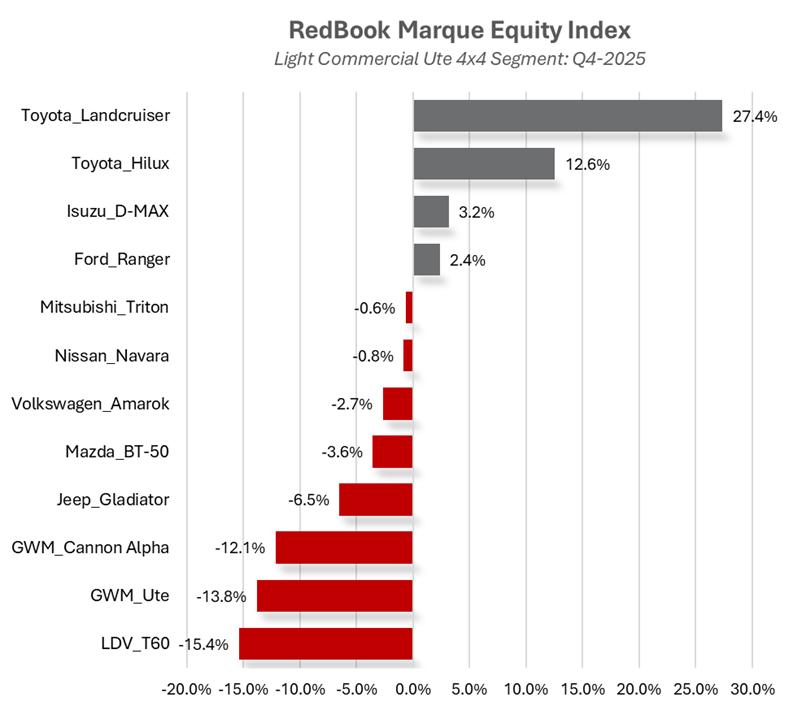

Segment Spotlight: Light Commercial Ute 4x4

This segment is a key indicator for fleet and trade buyers. LDV T60, GWM Ute, GWM Cannon Alpha, Jeep Gladiator, and Mazda BT-50 are underperforming, with LDV T60 at -15.4%. Toyota Landcruiser and Hilux remain benchmarks for value retention, leading with 27.4% and 12.6% respectively.

Over three years, Toyota Landcruiser has consistently led, while Isuzu D-MAX and Ford Ranger have shown positive growth. Mitsubishi Triton and Nissan Navara have experienced more volatility, reflecting the impact of product updates and market positioning.

Industry Insights & Takeaways

- Brand Resilience: Toyota’s consistent outperformance highlights the value of reputation, reliability, and dealer support.

- Emerging Challenges: Brands with negative MEI scores may need to reassess strategies.

- Premium Volatility: Luxury segment swings show the importance of exclusivity, innovation and a strong product line-up.

- Fleet Strategy: Understanding MEI trends is crucial for OEMs, fleet managers, and dealers.

Looking Ahead: Australian Opportunities and Challenges

As 2025 ends, Australia’s automotive landscape is evolving with shifting brand perceptions, new competition, strong consumer loyalty, and greater EV adoption. Adapting strategies and improving offerings will be key to staying competitive.

For more information or to subscribe, contact info@redbook.com.au.